All Categories

Featured

Table of Contents

Dealt with or variable development: The funds you add to delayed annuities can expand over time., the insurance coverage business sets a certain portion that the account will earn every year.

A variable annuity1, on the various other hand, is most often linked to the financial investment markets. The development might be even more than you would access a fixed price. It is not ensured, and in down markets the account might lose worth. No. An annuity is an insurance coverage item that can assist guarantee you'll never ever run out of retired life cost savings.

Both IRAs and annuities can help minimize that issue. Understanding the differences is key to making the most of your financial savings and intending for the retirement you are entitled to.

Annuities transform existing cost savings into ensured repayments. If you're not sure that your savings will certainly last as long as you need them to, an annuity is a good means to reduce that concern.

On the other hand, if you're a long means from retirement, beginning an IRA will certainly be advantageous. And if you have actually contributed the maximum to your IRA and wish to put additional cash towards your retired life, a deferred annuity makes good sense. If you're unclear concerning exactly how to manage your future cost savings, a financial specialist can assist you get a more clear image of where you stand.

Analyzing Fixed Income Annuity Vs Variable Annuity A Comprehensive Guide to Annuities Variable Vs Fixed Breaking Down the Basics of Investment Plans Benefits of Choosing the Right Financial Plan Why Choosing the Right Financial Strategy Can Impact Your Future Indexed Annuity Vs Fixed Annuity: A Complete Overview Key Differences Between Variable Annuity Vs Fixed Indexed Annuity Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About What Is A Variable Annuity Vs A Fixed Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Annuities Variable Vs Fixed A Beginner’s Guide to Smart Investment Decisions A Closer Look at Variable Vs Fixed Annuity

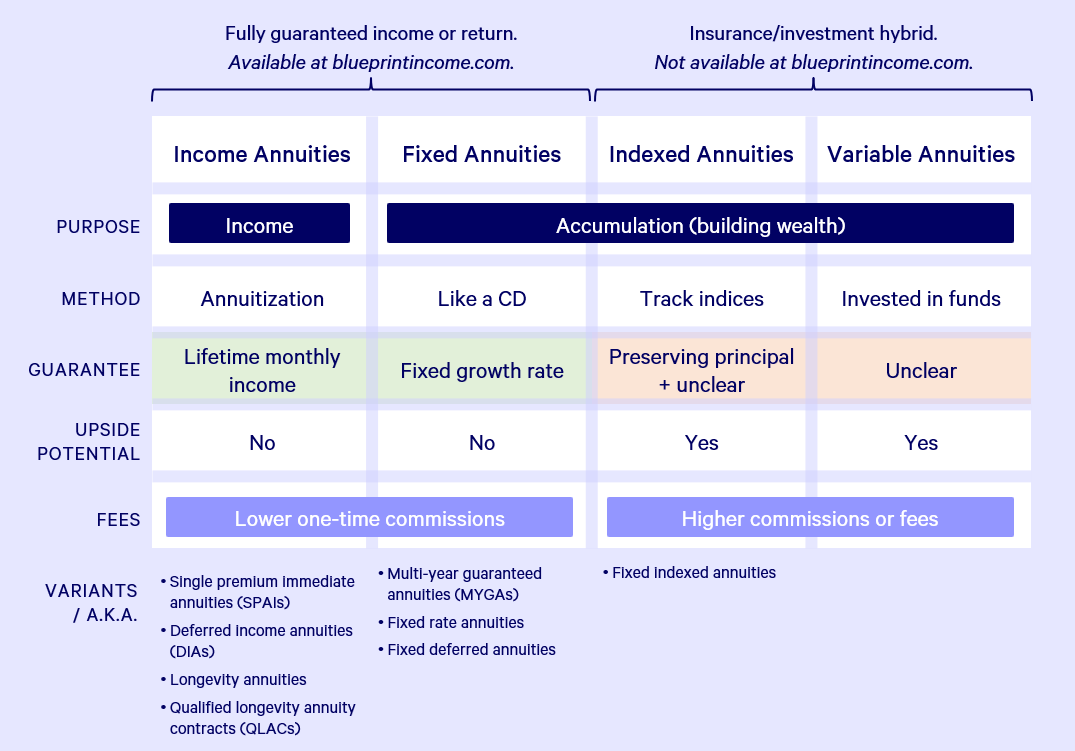

When thinking about retirement preparation, it is necessary to locate an approach that finest fits your lifefor today and in tomorrow. might assist ensure you have the revenue you need to live the life you want after you retire. While fixed and fixed index annuities audio similar, there are some crucial differences to arrange with prior to choosing the ideal one for you.

is an annuity contract made for retirement earnings that ensures a set rate of interest rate for a specific amount of time, such as 3%, despite market efficiency. With a set rate of interest price, you understand beforehand just how much your annuity will grow and just how much earnings it will pay out.

The earnings might be available in fixed repayments over an established number of years, taken care of repayments for the rest of your life or in a lump-sum payment. Revenues will not be taxed up until. (FIA) is a sort of annuity contract developed to create a steady retired life earnings and allow your properties to grow tax-deferred.

This creates the potential for more development if the index carries out welland conversely supplies security from loss as a result of inadequate index performance. Although your annuity's interest is linked to the index's efficiency, your cash is not straight purchased the market. This means that if the index your annuity is linked to does not do well, your annuity doesn't shed its worth as a result of market volatility.

Set annuities have actually a guaranteed minimum rate of interest rate so you will certainly receive some passion each year. Set annuities might have a tendency to position much less economic risk than other kinds of annuities and investment products whose worths rise and drop with the market.

And with particular sorts of fixed annuities, like a that set rates of interest can be locked in with the entire contract term. The interest made in a taken care of annuity isn't influenced by market fluctuations for the period of the fixed period. Similar to many annuities, if you want to withdraw money from your fixed annuity earlier than set up, you'll likely sustain a fine, or give up chargewhich in some cases can be significant.

Exploring the Basics of Retirement Options Key Insights on Pros And Cons Of Fixed Annuity And Variable Annuity What Is Annuity Fixed Vs Variable? Pros and Cons of Various Financial Options Why Annuities Variable Vs Fixed Is Worth Considering How to Compare Different Investment Plans: How It Works Key Differences Between Different Financial Strategies Understanding the Rewards of Long-Term Investments Who Should Consider Pros And Cons Of Fixed Annuity And Variable Annuity? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Additionally, withdrawals made before age 59 may undergo a 10 percent government tax obligation penalty based on the fact the annuity is tax-deferred. The passion, if any type of, on a fixed index annuity is tied to an index. Since the rate of interest is tied to a stock market index, the passion credited will either advantage or suffer, based on market efficiency.

You are trading potentially gaining from market growths and/or not equaling rising cost of living. Dealt with index annuities have the advantage of possibly offering a higher guaranteed rate of interest rate when an index performs well, and major protection when the index experiences losses. For this defense against losses, there might be a cap on the maximum earnings you can get, or your incomes might be restricted to a portion (as an example, 70%) of the index's readjusted value.

It usually also has an existing rates of interest as stated by the insurer. Passion, if any type of, is linked to a defined index, as much as a yearly cap. A product might have an index account where interest is based on just how the S&P 500 Index carries out, subject to an annual cap.

This feature shields versus the threat of market losses. It likewise restricts possible gains, also when the market is up. Passion gained depends on index performance which can be both positively and adversely impacted. Along with understanding dealt with annuity vs. fixed index annuity differences, there are a couple of other kinds of annuities you may want to discover prior to choosing.

{kind=link}

Table of Contents

Latest Posts

Breaking Down Deferred Annuity Vs Variable Annuity Everything You Need to Know About Variable Annuity Vs Fixed Indexed Annuity Defining Fixed Index Annuity Vs Variable Annuities Benefits of Annuities

Understanding Fixed Income Annuity Vs Variable Annuity A Comprehensive Guide to Variable Vs Fixed Annuities Breaking Down the Basics of Variable Annuity Vs Fixed Annuity Benefits of Choosing the Right

Highlighting the Key Features of Long-Term Investments A Closer Look at Fixed Vs Variable Annuity Pros Cons Breaking Down the Basics of Annuity Fixed Vs Variable Advantages and Disadvantages of Variab

More

Latest Posts